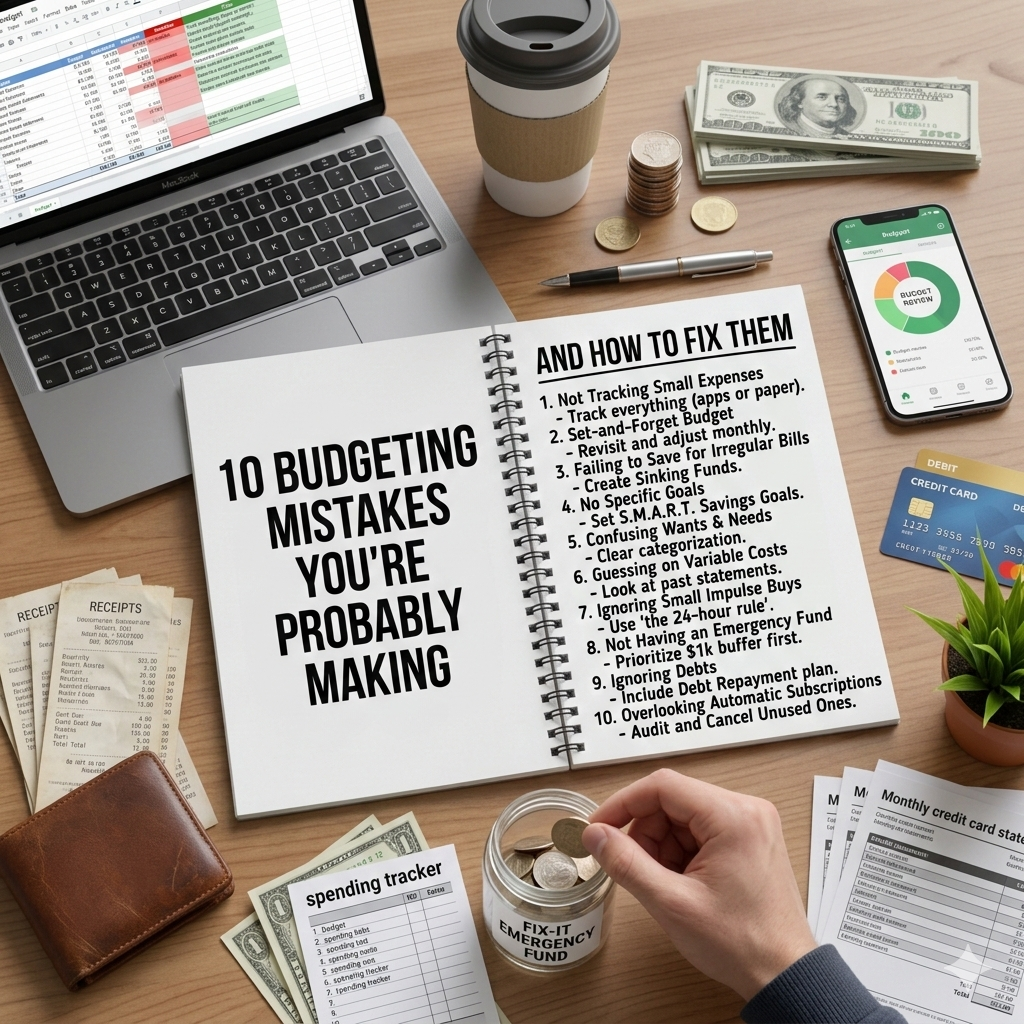

10 Budgeting Mistakes You’re Probably Making(And How To Fix Them)

Most budgets dont fail because of lack of discipline — they fail because of avoidable mistakes . Here are 10 most common budgeting mistakes and exactly how to fix them

Budgeting sounds straightforward — track your income, track your expenses, spend less than you earn. Simple in theory. Much harder in practice. And the reason most budgets fail isn't lack of effort or discipline — it's a handful of common, avoidable mistakes that silently sabotage even the best intentions.

If you've tried budgeting before and it didn't stick, chances are one or more of these mistakes is the reason. Here are the 10 most common budgeting mistakes people make — and exactly how to fix them.

1. Not Having a Budget at All

The most common budgeting mistake is not budgeting in the first place. Many people believe they have a rough idea of where their money goes — but a rough idea is not a budget. Without a clear, written plan for your money, spending decisions happen by default rather than by design.

Studies consistently show that people who budget accumulate significantly more savings than those who don't — even at the same income level. The act of writing down a budget forces awareness and creates accountability that mental tracking simply cannot replicate.

The fix: Start with a simple one-page budget. Write down your income, your fixed expenses, your variable spending categories, and your savings target. It doesn't need to be perfect — it just needs to exist.

2. Forgetting Irregular Expenses

This is one of the most budget-busting mistakes people make. You carefully plan your monthly expenses — rent, groceries, phone bill, subscriptions — and everything looks balanced. Then the car needs servicing. Or an annual insurance premium arrives. Or a birthday, a wedding, or a holiday comes around. Suddenly your budget is blown and you can't figure out why.

Irregular expenses are predictable — they happen every year. The mistake is failing to account for them monthly.

The fix: List every irregular expense you know is coming in the next 12 months — annual subscriptions, car maintenance, medical costs, gifts, travel, school fees. Add up the total and divide by 12. Add that monthly amount to your budget as a dedicated "irregular expenses" category and set it aside each month.

3. Being Too Restrictive

A budget that allows for no fun, no treats, and no flexibility is a budget that won't last more than a few weeks. Many people approach budgeting with a punishment mindset — cutting everything enjoyable in a desperate bid to save more. It feels disciplined at first. Then real life happens, willpower runs out, and the whole budget gets abandoned in a moment of frustration.

The fix: Build a "personal spending" or "fun money" category into your budget deliberately. Give yourself a realistic, guilt-free allowance for enjoyment every month. A budget that includes fun is a budget you'll actually stick to.

4. Saving Whatever Is Left Over

If your approach to saving is "I'll save whatever is left at the end of the month," you will almost never save anything. There is rarely anything left at the end of the month — because money expands to fill the space available to it. This is known as Parkinson's Law applied to finance, and it affects almost everyone who doesn't budget intentionally.

The fix: Pay yourself first. As soon as money arrives in your account, transfer your savings amount immediately — before you pay bills, before you buy groceries, before you do anything else. Treat savings as your first and most important expense, not your last.

5. Not Tracking Your Actual Spending

Creating a budget is step one. Tracking whether you're actually sticking to it is step two — and most people skip it entirely. A budget you never check is just a wish list. Without tracking, you have no idea whether you're on target or overspending until the damage is already done.

The fix: Review your spending at least once a week — not once a month. Weekly check-ins catch problems early, when you still have time to course-correct. Use a spreadsheet, a budgeting app, or even a notebook. The tool doesn't matter. The habit does.

6. Setting Unrealistic Spending Limits

Budgeting $100 per month for groceries when you actually spend $350 isn't discipline — it's wishful thinking. Unrealistic budget categories are set with good intentions but are impossible to maintain, which leads to a cascade of guilt, frustration, and eventually abandonment of the entire budget.

The fix: Before setting any spending limits, go through two to three months of bank statements and calculate what you actually spend in each category. Use those real numbers as your starting point. Then make gradual, realistic reductions — not dramatic cuts that are impossible to sustain.

7. Ignoring Small Purchases

A $4 coffee. A $2 app. A $6 snack. A $3 parking fee. Individually, these feel too small to worry about. Collectively, they can easily add up to $100–$200 per month — money that disappears without any awareness or intention. This is sometimes called the "latte factor," and while it's been debated, the core principle holds: small, habitual purchases add up significantly over time.

The fix: Track every purchase for at least two weeks — including the small ones. Most people are genuinely surprised by what they find. You don't necessarily need to eliminate all small purchases, but you should be making them consciously rather than automatically.

8. Not Adjusting Your Budget When Life Changes

A budget built six months ago may no longer reflect your current reality. Income changes, rent goes up, a new expense arrives, a subscription gets cancelled. Using an outdated budget is like navigating with an old map — you'll keep ending up somewhere you didn't intend to go.

The fix: Review and update your budget every month. The monthly review should be a fixed habit — 15 minutes at the start or end of each month to update categories, adjust limits, and realign your plan with your current life. Your budget should always reflect reality, not a version of your life that no longer exists.

9. Budgeting as a Couple Without Communicating

Money is one of the leading causes of relationship conflict — and much of that conflict stems from partners having different spending habits, different financial priorities, and no shared budget or financial plan. When one person is saving aggressively and the other is spending freely, resentment builds fast.

The fix: If you share finances with a partner, build the budget together. Have an honest conversation about your financial goals, your individual spending habits, and how you want to manage money as a team. Schedule a regular "money date" — a monthly check-in where you review your budget together. It removes secrecy and builds financial alignment.

10. Giving Up After One Bad Month

This might be the most damaging budgeting mistake of all. You overspend in one category. Life throws an unexpected expense at you. You have a stressful week and spend more than planned. And instead of resetting and continuing, you decide that budgeting "doesn't work" and abandon the whole thing.

One bad month is not a failure. It's data. Every experienced budgeter has off months. The difference between people who succeed with budgeting and those who don't is not that the successful ones never overspend — it's that they don't let one overspend become a reason to quit.

The fix: Adopt a "reset and continue" mindset. At the start of each new month, your budget resets. Whatever happened last month is in the past. The only question is what you're going to do differently this month. Progress over perfection, always.

Quick Summary: 10 Budgeting Mistakes and Their Fixes

- No budget at all — Start a simple one-page budget today

- Forgetting irregular expenses — Divide annual costs by 12 and budget monthly

- Being too restrictive — Include a fun money category deliberately

- Saving whatever is left — Pay yourself first, every payday

- Not tracking spending — Check in with your budget weekly

- Unrealistic spending limits — Base limits on real spending data

- Ignoring small purchases — Track everything for two weeks

- Not updating your budget — Review and adjust every month

- No financial communication with partner — Budget together, check in monthly

- Quitting after one bad month — Reset and continue, every time

The Bottom Line

Budgeting doesn't fail because it's a bad idea. It fails because of specific, identifiable mistakes that can all be fixed with small adjustments to your approach. The fact that you're reading this means you're already more financially aware than most people.

Pick the one or two mistakes on this list that resonate most with your experience. Fix those first. Build from there. Budgeting is a skill — and like any skill, it gets easier and more effective the longer you practise it.

Your finances are worth the effort. Keep going.

Which of these mistakes have you made before? Be honest in the comments — you're definitely not alone, and sharing might help someone else recognise the same pattern in their own budget.

Related Posts

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

0 Comments

No comments yet. Be the first to comment!

Leave a comment

Trending News

Newsletter

Stay updated with the latest personal finance and money tips.