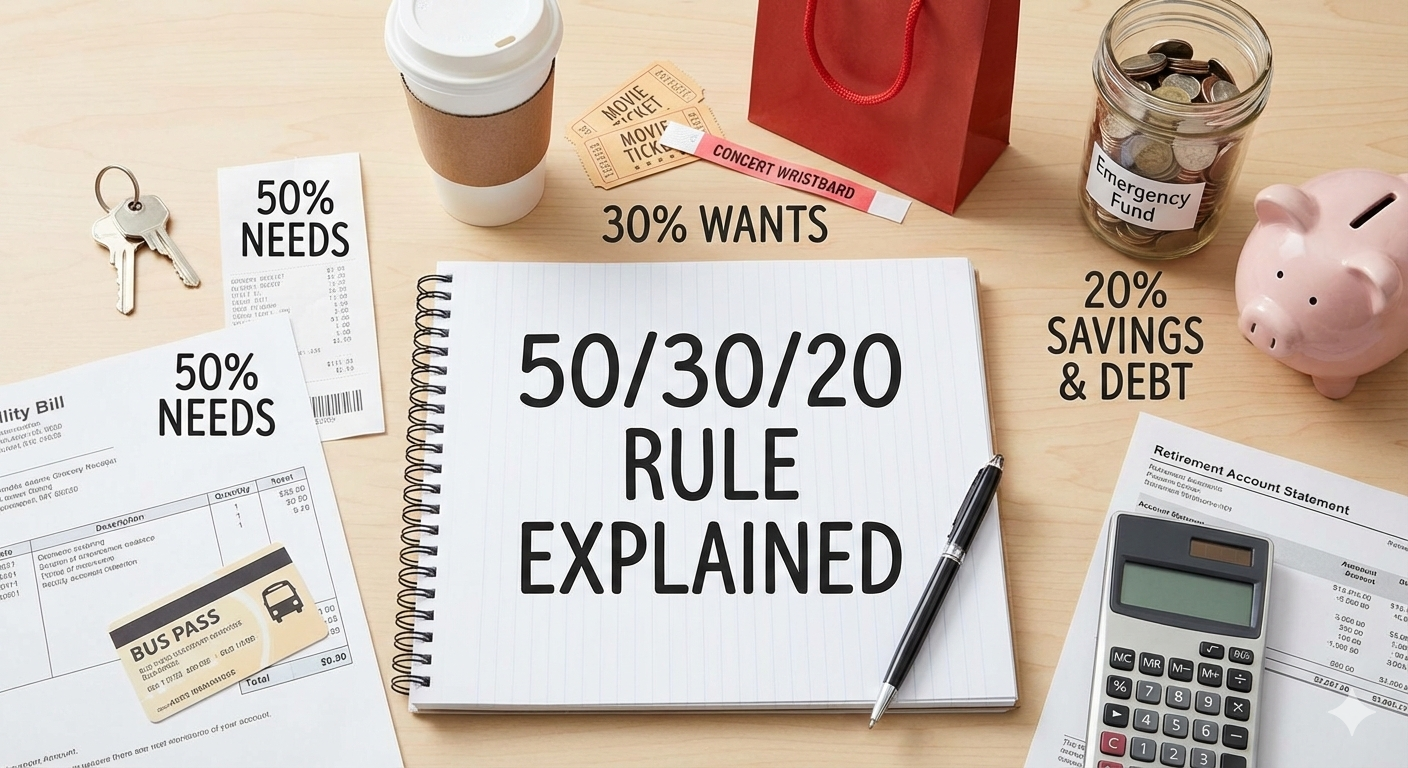

50/30/20 Budget Rule Explained: Is it Right For You?

50/30/20 rule is one of the simplest budgeting methods out there. But is it right for your situation? Here’s everything you need to know.

If you've ever searched for a simple way to manage your money, chances are you've come across the 50/30/20 rule. It's one of the most popular budgeting frameworks in the world — and for good reason. It's straightforward, flexible, and works for people at almost every income level.

But is it right for you? And how exactly do you apply it to your own finances?

In this post, we break down the 50/30/20 rule in full — what it means, how to use it, its pros and cons, and how to adapt it to your real life.

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting method that divides your after-tax income into three broad categories:

- 50% on Needs — the essentials you can't live without

- 30% on Wants — the things that make life enjoyable but aren't strictly necessary

- 20% on Savings and Debt Repayment — building your financial future

The rule was popularised by US Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan. The core idea is simple: instead of tracking every single penny, you manage your money in three broad buckets. Less stress, more clarity.

Breaking Down Each Category

50% — Needs

Needs are expenses that are essential to your basic survival and functioning. If you didn't pay them, there would be serious consequences. These include:

- Rent or mortgage payments

- Utility bills (electricity, water, gas)

- Groceries and basic food

- Transport to work (fuel, public transport)

- Minimum debt repayments

- Basic insurance (health, car if required)

- Phone and internet (if needed for work)

The key word here is essential. A roof over your head is a need. A premium apartment in the most expensive part of town is partly a want. Be honest with yourself when categorising.

30% — Wants

Wants are the non-essential expenses that improve your quality of life but that you could technically live without. These include:

- Dining out and takeaways

- Entertainment (streaming services, concerts, cinema)

- Gym memberships and hobbies

- Shopping for clothes beyond basics

- Holidays and travel

- Upgrading to a nicer phone, car, or home than you strictly need

- Subscriptions you enjoy but don't need

This category is not about guilt. Wants are a legitimate and important part of your budget. The 50/30/20 rule explicitly allocates 30% to them — because a budget that has no room for enjoyment is a budget you won't stick to.

20% — Savings and Debt Repayment

This is the category that builds your financial future. It includes:

- Emergency fund contributions

- Retirement savings or pension contributions

- Investments (stocks, index funds, etc.)

- Paying off debt above the minimum (e.g. credit cards, student loans)

- Saving for specific goals (house deposit, car, education)

Note that minimum debt repayments go under Needs (you have no choice but to pay them). Extra debt repayments — paying more than the minimum to clear debt faster — go here under the 20%.

How to Apply the 50/30/20 Rule: A Step-by-Step Example

Let's say your monthly after-tax income is $3,000. Here's how the rule applies:

- 50% Needs: $1,500 — rent, bills, groceries, transport

- 30% Wants: $900 — dining out, entertainment, hobbies, subscriptions

- 20% Savings: $600 — emergency fund, investments, extra debt payments

Now let's say your monthly after-tax income is $5,000:

- 50% Needs: $2,500

- 30% Wants: $1,500

- 20% Savings: $1,000

The percentages stay the same regardless of income. That's part of what makes this method so universally applicable.

What If My Needs Are More Than 50%?

This is the most common challenge people face — especially in high cost-of-living cities or on lower incomes. Rent alone can eat up more than 50% of take-home pay for many people.

If your needs genuinely exceed 50%, here's what to do:

- First, audit your "needs". Are all of them truly essential? Could you switch to a cheaper phone plan, find a flatmate, or cut a bill you've been overpaying?

- Adjust the percentages. The 50/30/20 rule is a guideline, not a law. If your needs are 60%, scale back wants to 20% and keep savings at 20%. The savings target is the one to protect most.

- Work on increasing income. If expenses are unavoidable and income is the constraint, focus on growing what's coming in — a side hustle, a raise, or a better-paying role.

The rule is a framework. Real life requires flexibility.

Pros of the 50/30/20 Rule

- Simple and easy to follow — no need to track 20 different spending categories

- Flexible — works across different income levels and lifestyles

- Guilt-free spending — explicitly allows for wants, reducing the feeling of deprivation

- Great starting point — ideal for budgeting beginners who feel overwhelmed by detailed tracking

- Savings are built in — the 20% means you're always making financial progress

Cons of the 50/30/20 Rule

- Too broad for some people — if you need detailed visibility into your spending, three buckets might not give you enough information

- The 30% wants allowance can be too generous — especially if you're trying to aggressively pay off debt or save for a big goal

- Doesn't work well on very low incomes — when 70–80% of income goes to essentials, the structure breaks down

- Needs vs wants can be blurry — a car might be a need for someone in a rural area but a want for someone in a city with great public transport

Who Is the 50/30/20 Rule Best For?

The 50/30/20 rule works best for:

- People who are new to budgeting and want a simple framework to start with

- Those with a stable, predictable income

- Anyone who finds detailed expense tracking too tedious to maintain

- People who are broadly on track financially but want more structure

It may not be the best fit if you're in significant debt and need to aggressively pay it down, if your income is highly variable, or if you're saving for a specific short-term goal that requires a higher savings rate.

Adapting the Rule to Your Situation

The beauty of the 50/30/20 rule is that the percentages are adjustable. Some common variations:

- Aggressive debt payoff: 50% needs / 20% wants / 30% debt + savings

- High savings goal: 50% needs / 20% wants / 30% savings

- High cost-of-living area: 60% needs / 20% wants / 20% savings

- Lower income, building up: 70% needs / 10% wants / 20% savings

The core principle remains the same: intentionally allocate your income across essentials, lifestyle, and the future — and adjust the ratios to fit where you actually are in life.

The Bottom Line

The 50/30/20 rule is one of the most effective budgeting frameworks available precisely because it's simple. It removes the overwhelm of tracking every transaction and replaces it with three clear, manageable categories.

Is it perfect for everyone? No. But as a starting framework — especially if you've never budgeted before — it's hard to beat. Give it one month. See where your money is actually going. Then tweak the percentages to suit your life.

Financial control doesn't have to be complicated. Sometimes three numbers are all you need.

Are you currently using the 50/30/20 rule, or are you thinking of trying it? Let us know in the comments — and feel free to share what percentages work best for your situation.

Related Posts

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

0 Comments

No comments yet. Be the first to comment!

Leave a comment

Trending News

Newsletter

Stay updated with the latest personal finance and money tips.