How to Create a Budget that Actually Works (Step by Step Guide)

A good budget doesn’t Strick your life— It gives you control over it. Here’s a simple, step by step guide to creating a budget that you’ll actually stick to.

Most people know they should have a budget. Far fewer actually have one that works. And if you've ever tried budgeting only to give up a few weeks later, you're not alone — the problem usually isn't discipline. It's that the budget wasn't built the right way in the first place.

A good budget doesn't restrict your life. It gives you control over it. It tells your money where to go instead of wondering where it went.

In this guide, we'll walk you through exactly how to create a budget that actually works — step by step, from scratch. No complicated spreadsheets. No financial degree required.

What Is a Budget and Why Do You Need One?

A budget is simply a plan for your money. It's a breakdown of how much you earn, how much you spend, and how much you save — and a decision about how you want those numbers to look going forward.

Without a budget, most people spend reactively. They pay bills when they arrive, buy things when they want them, and save whatever happens to be left — which is usually nothing. A budget flips that script. You decide in advance where every pound, dollar, or naira goes.

The benefits go beyond just saving more money. Budgeting reduces financial stress, helps you reach goals faster, prevents debt from creeping up on you, and gives you a clear picture of your financial health at any moment.

Step 1: Calculate Your Total Monthly Income

Start with what's coming in. Add up all sources of income you receive each month:

- Your salary or wages (after tax)

- Freelance or side hustle income

- Rental income

- Any government benefits or allowances

- Any other regular income

If your income varies month to month, use a conservative average — base it on your three lowest-earning months over the past year. It's always better to underestimate income than to overestimate it.

This number is your starting point. Everything else in your budget flows from here.

Step 2: List All Your Monthly Expenses

Now write down everything you spend money on. Be thorough — this is where most budgets fail. People forget irregular expenses and then wonder why their budget keeps falling apart.

Split your expenses into two categories:

Fixed expenses — these are the same every month:

- Rent or mortgage

- Loan repayments

- Insurance premiums

- Subscriptions (Netflix, Spotify, gym, etc.)

- Phone and internet bills

Variable expenses — these change month to month:

- Groceries

- Transport and fuel

- Eating out and entertainment

- Clothing and personal care

- Household supplies

Also account for irregular expenses — things that don't happen every month but are predictable: car servicing, annual subscriptions, birthdays, school fees, medical costs. Divide their yearly total by 12 and add that amount as a monthly line item. This alone prevents a lot of budget busting.

Step 3: Subtract Expenses From Income

Now do the maths. Take your total monthly income and subtract your total monthly expenses.

Three outcomes are possible:

- Positive number: You have money left over. This is your opportunity to save, invest, or pay off debt faster.

- Zero: Every pound is accounted for. This is intentional with zero-based budgeting — and it works well if savings are already built into your expenses.

- Negative number: You're spending more than you earn. This needs to be fixed immediately, either by cutting expenses or increasing income.

Whatever the result, seeing it clearly is the first step to improving it.

Step 4: Choose a Budgeting Method

There's no single "right" way to budget. The best method is the one you'll actually stick to. Here are the three most popular approaches:

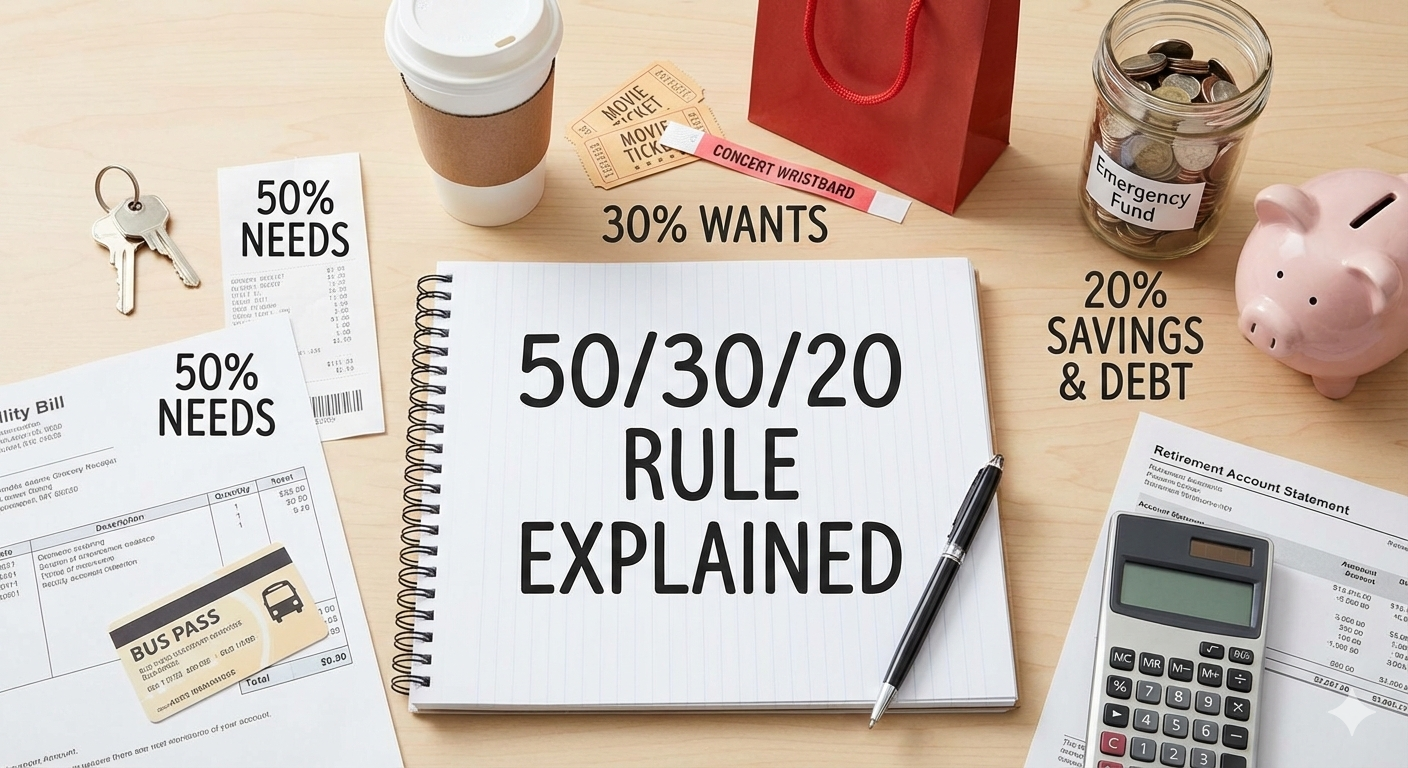

The 50/30/20 Rule

Split your after-tax income into three categories: 50% for needs (rent, food, bills), 30% for wants (entertainment, dining out, hobbies), and 20% for savings and debt repayment. It's simple, flexible, and great for beginners. The percentages can be adjusted to suit your situation.

Zero-Based Budgeting

Give every single pound or dollar a job until your income minus your expenses equals zero. You're not spending everything — savings and investments count as expenses in this system. It requires more attention but gives you complete control over your money.

The Envelope Method

Allocate cash to physical (or digital) envelopes for each spending category. When the envelope is empty, spending in that category stops for the month. It's highly effective for people who tend to overspend on discretionary items like food and entertainment.

Pick one, try it for a month, and adjust from there.

Step 5: Set Your Savings Goal First

Before you allocate money to spending, decide how much you want to save each month. Treat savings as a non-negotiable expense — not an afterthought.

A common starting point is 20% of your income, but any amount is better than nothing. If 20% feels impossible right now, start with 5% or even 2%. The habit matters more than the amount in the early stages.

What are you saving for? An emergency fund should be your first priority — aim for three to six months of essential expenses. After that, you can direct savings toward specific goals: a holiday, a car, a house deposit, or investments.

Step 6: Track Your Spending Throughout the Month

Creating a budget is step one. Sticking to it requires tracking. Check in with your budget regularly — ideally weekly — to see how your actual spending compares to your plan.

You don't need anything fancy to do this. Options include:

- A spreadsheet — Google Sheets or Excel work perfectly. Simple and free.

- A budgeting app — apps like YNAB, Mint, or Money Manager can link to your accounts and track spending automatically.

- Pen and paper — old-fashioned but effective, especially if you're just starting out.

The tool doesn't matter. Consistency does. If you track your spending every week, you'll spot problems early — before they blow your budget entirely.

Step 7: Review and Adjust Every Month

At the end of each month, sit down with your budget for 15 minutes and ask yourself:

- Did I stick to my spending categories?

- Where did I overspend, and why?

- Did I hit my savings target?

- Do any categories need adjusting for next month?

A budget is a living document. Your income changes, your expenses shift, your goals evolve. The monthly review keeps your budget relevant and keeps you honest. Most people who "fail" at budgeting simply stopped reviewing and adjusting — they didn't actually fail at the concept.

Common Budgeting Mistakes to Avoid

Even with the best intentions, it's easy to fall into these traps:

- Being too strict: A budget with zero room for fun is a budget you'll abandon. Build in a "personal spending" or "fun money" category so you don't feel deprived.

- Forgetting irregular expenses: Car repairs, annual bills, and seasonal costs will wreck a budget that doesn't account for them. Plan ahead.

- Giving up after one bad month: One overspend doesn't mean budgeting doesn't work. Reset and start fresh next month.

- Not tracking at all: Creating a budget without tracking your spending is like setting a destination without checking whether you're on the right road.

Simple Budget Template to Get You Started

Here's a basic structure you can adapt to your own numbers:

Monthly Income: [Your total after-tax income]

Fixed Expenses:

- Rent/Mortgage: $_____

- Loan repayments: $_____

- Insurance: $_____

- Phone/Internet: $_____

- Subscriptions: $_____

Variable Expenses:

- Groceries: $_____

- Transport: $_____

- Eating out: $_____

- Entertainment: $_____

- Personal care: $_____

- Clothing: $_____

Savings:

- Emergency fund: $_____

- Goal savings: $_____

Total Expenses + Savings: $_____

Remaining (should be zero or positive): $_____

The Bottom Line

Budgeting isn't about being perfect with money. It's about being intentional. When you know where your money is going — and you've decided in advance where you want it to go — you're already ahead of the majority of people.

Start simple. Pick a method. Track your spending. Review it monthly. Adjust as you go.

Your first budget won't be perfect, and that's completely fine. The point is to start — and to keep going.

Have you tried budgeting before? What's worked for you and what hasn't? Share in the comments below — we'd love to hear from you.

Related Posts

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

0 Comments

No comments yet. Be the first to comment!

Leave a comment

Trending News

Newsletter

Stay updated with the latest personal finance and money tips.