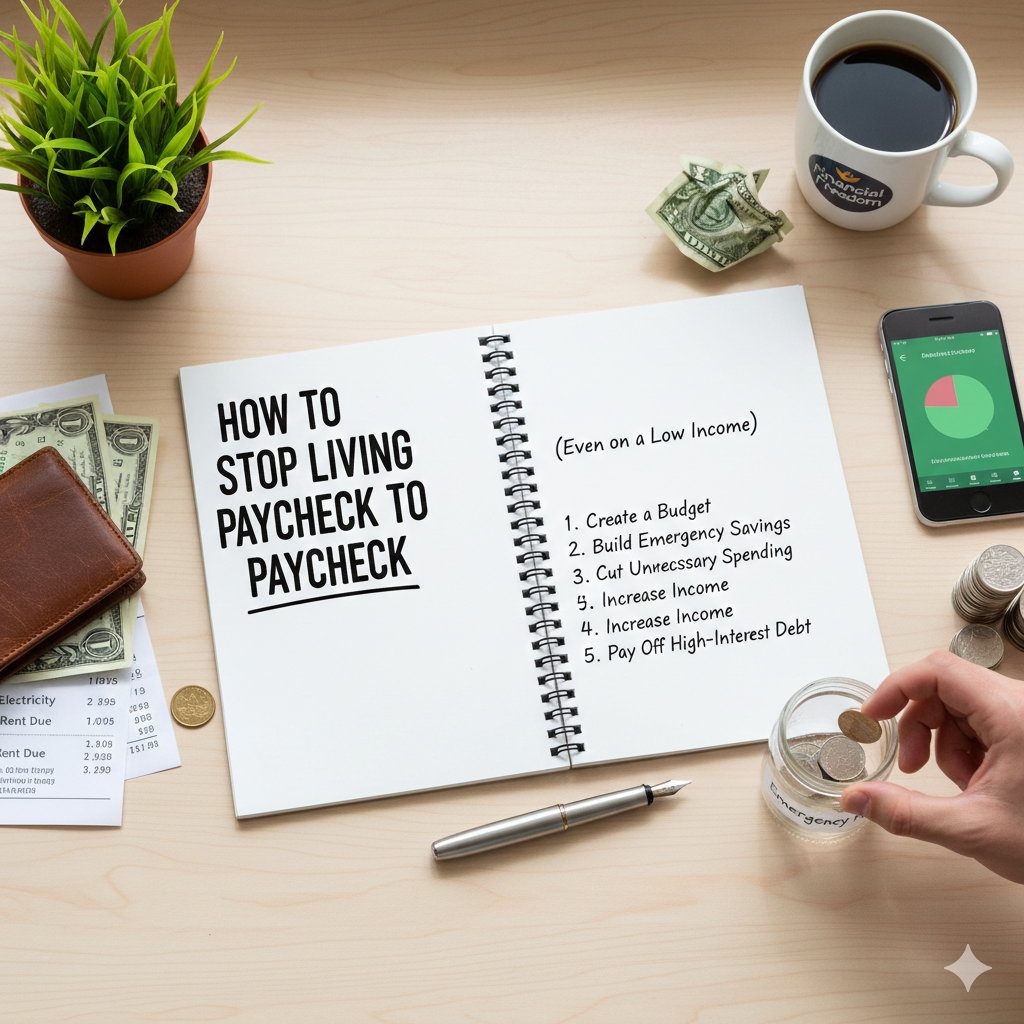

How to Stop Living Paycheck to Paycheck (Even on a Low Income)

Breaking the paycheck-to-paycheck cycle isn't about earning more — it's about managing what you have better. Here's a step-by-step plan that actually works.

Living paycheck to paycheck is more common than most people admit. You earn money, bills arrive, life happens, and by the time the next payday comes around, there's little to nothing left. It's a cycle that feels impossible to break — but it isn't.

The good news is that escaping the paycheck-to-paycheck trap doesn't require a dramatic income increase or a complete lifestyle overhaul. It requires a shift in how you manage the money you already have. This guide will show you exactly how to do that — step by step, even on a low income.

Why the Paycheck-to-Paycheck Cycle Is So Hard to Break

Before we look at solutions, it helps to understand what keeps people stuck. The paycheck-to-paycheck cycle persists for a few key reasons:

- No financial buffer. Without savings, any unexpected expense — a medical bill, a car repair, a broken appliance — immediately becomes a crisis that wipes out next month's budget too.

- Lifestyle creep. As income increases, spending tends to increase at the same rate. More money comes in, more goes out, and nothing is saved.

- No clear picture of where money goes. Most people living paycheck to paycheck have never actually tracked their spending. They know money disappears — they don't know exactly where.

- Debt payments eating income. Monthly debt repayments — credit cards, loans, buy-now-pay-later — consume a significant portion of income before there's any chance to save.

Understanding the cause helps you target the right solution. Let's get into it.

Step 1: Get an Honest Picture of Your Money

You can't fix a problem you haven't clearly defined. The first step is to sit down and get completely honest about your financial situation — income, expenses, and debt.

Write down:

- Your total monthly take-home income from all sources

- Every monthly expense — fixed bills, variable spending, subscriptions, debt repayments

- Your total debt — what you owe, to whom, and at what interest rate

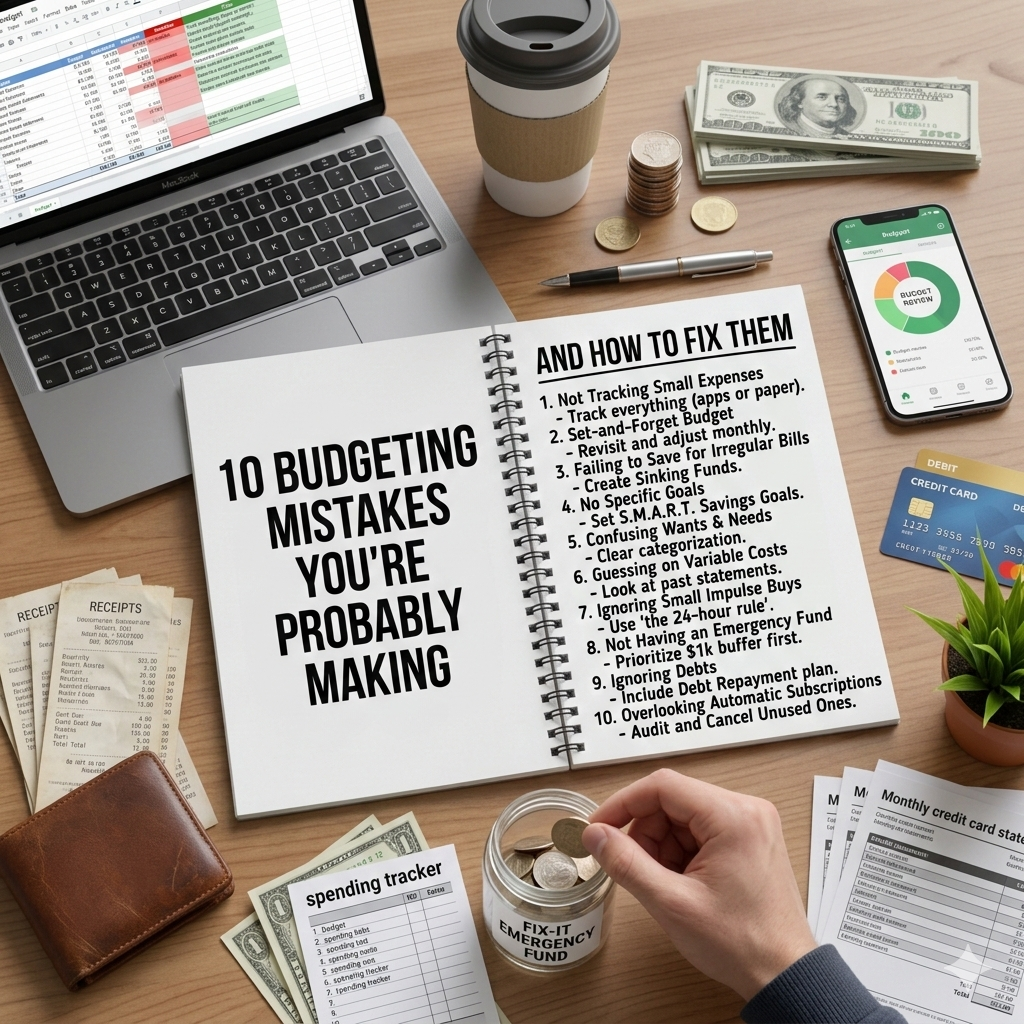

Go through your last two or three months of bank statements to make sure you haven't missed anything. Most people are surprised by what they find — forgotten subscriptions, habitual small purchases that add up significantly, and expenses they'd mentally categorised as smaller than they actually are.

This exercise alone is often enough to spark immediate change.

Step 2: Find the Gaps and Plug Them

Once you have a clear picture of your income and expenses, calculate the difference. If you're spending more than you earn, you have a deficit that needs addressing immediately. If your income and expenses are roughly equal, you have no buffer — and one unexpected expense away from crisis.

Look for spending you can reduce or eliminate right now:

- Subscriptions you barely use — streaming services, apps, gym memberships, magazines. Cancel anything you haven't used in the past month.

- Food spending — eating out, takeaways, and coffee runs are often the biggest discretionary drain on a tight budget. Cooking at home more often makes a noticeable difference quickly.

- Impulse purchases — small, unplanned purchases are budget killers. Introduce a 24-hour rule before buying anything non-essential.

- Unused services — review insurance policies, phone plans, and utility providers. Many people are on plans that no longer suit them and are overpaying as a result.

The goal is to create a gap between what you earn and what you spend. That gap is where financial stability begins.

Step 3: Build a Micro Emergency Fund First

Before focusing on anything else — debt payoff, investing, or bigger savings goals — build a small emergency fund of $500 to $1,000. This is your financial firewall.

Without any savings buffer, every unexpected expense forces you to borrow — credit cards, loans, borrowing from family — which deepens the cycle. With even a small emergency fund, you can handle most common financial surprises without derailing your entire budget.

Treat this savings goal as urgent. Sell unused items, take on a small amount of extra work, cut spending temporarily. Get to $500–$1,000 as fast as you can and keep it in a separate account you don't touch unless it's a genuine emergency.

Once you have this buffer, everything else becomes more manageable.

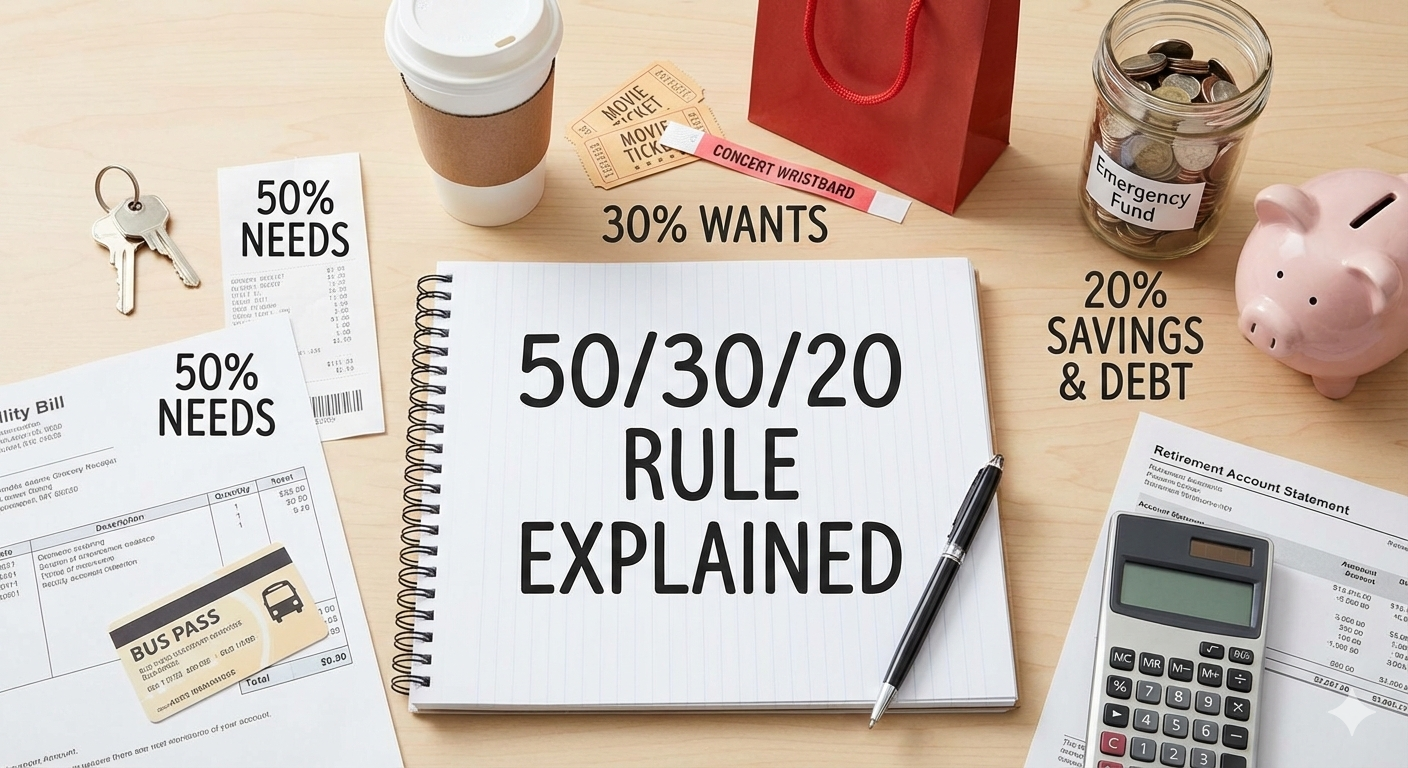

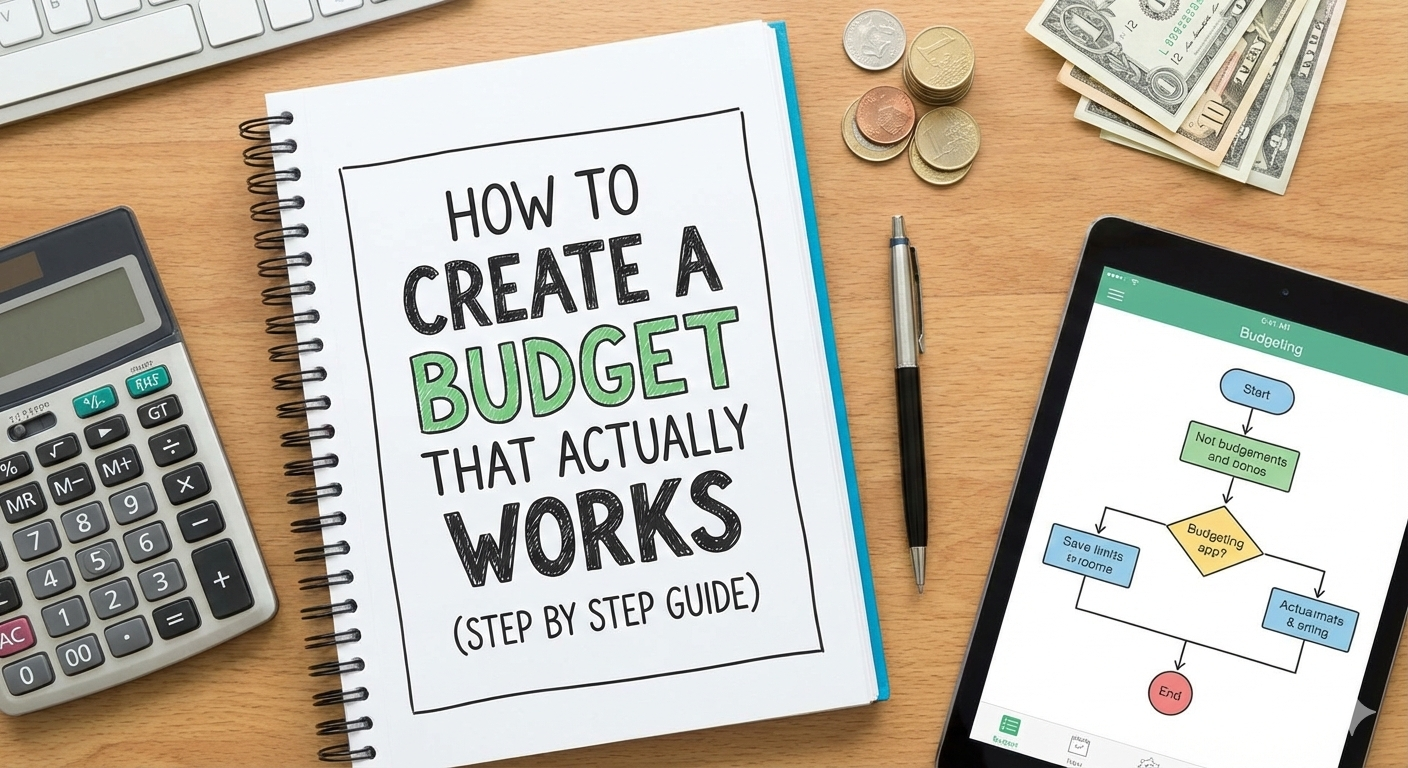

Step 4: Set Up a Simple Budget and Actually Use It

A budget is the single most powerful tool for stopping the paycheck-to-paycheck cycle. It tells your money where to go before it arrives — instead of wondering where it went after it disappears.

Keep it simple. A basic budget has three parts:

- Fixed essentials — rent, utilities, loan minimums, insurance. These are non-negotiable.

- Variable spending — groceries, transport, personal care. Set a realistic limit for each category.

- Savings — treat this as a fixed expense, not an afterthought. Even saving 3–5% of your income is a meaningful start.

Review your budget at the end of each week. Not at the end of the month — by then it's too late to course-correct. Weekly check-ins catch overspending early and keep you accountable throughout the month.

Step 5: Automate Your Savings

The reason most people fail to save is that they rely on willpower to transfer money manually after spending. By the time they think about saving, the money is already gone.

Automation removes willpower from the equation entirely. Set up an automatic transfer from your main account to a separate savings account on the day you get paid — before you have a chance to spend it. Even $20 or $30 per payday adds up over time, and you'll quickly adapt your spending to what remains.

Out of sight, out of mind works powerfully in your favour when it comes to saving.

Step 6: Tackle Debt Strategically

High-interest debt — particularly credit cards — is one of the most significant drivers of the paycheck-to-paycheck cycle. Interest charges consume money every month that could otherwise go toward savings or living expenses.

Two proven strategies for paying off debt:

- The Debt Snowball: Pay minimums on all debts and throw every extra pound or dollar at the smallest debt first. When it's cleared, roll that payment to the next smallest. The psychological momentum of clearing debts keeps you motivated.

- The Debt Avalanche: Pay minimums on all debts and focus extra payments on the highest-interest debt first. Mathematically faster and cheaper than the snowball — you pay less total interest overall.

Either method works. The best one is the one you'll actually stick to. As each debt is cleared, your monthly cash flow improves and the cycle becomes easier to break.

Step 7: Look for Ways to Increase Your Income

Cutting expenses has limits — you can only cut so much before quality of life suffers. Increasing income has no ceiling. Even a modest increase in monthly income, directed entirely toward savings or debt, can dramatically accelerate your progress.

Options worth considering:

- Ask for a raise at your current job — especially if you haven't had one in over a year

- Start a small side hustle — freelancing, tutoring, selling products online, offering a local service

- Sell unused items — clothes, electronics, furniture, books. A clear-out of your home can generate a few hundred pounds or dollars quickly.

- Explore better-paying job opportunities — sometimes the fastest income increase comes from a move to a new employer

Direct any additional income straight to your emergency fund or highest-interest debt first. Don't let a income increase trigger lifestyle creep — that's what keeps the cycle going.

Step 8: Change Your Relationship With Money

Breaking the paycheck-to-paycheck cycle isn't just about tactics — it also requires a shift in mindset. Some changes that make a lasting difference:

- Stop treating payday as permission to spend. Money arriving in your account is not an invitation to spend it — it's an opportunity to allocate it intentionally.

- Delay gratification deliberately. Practice waiting before buying. Most impulse purchases feel much less urgent after 24–48 hours.

- Measure spending in hours worked. Before buying something non-essential, ask yourself how many hours of work it cost. This reframes spending decisions powerfully.

- Celebrate saving as much as spending. Reaching a savings milestone deserves the same satisfaction as a purchase. Rewire how you think about what "treating yourself" means.

How Long Does It Take to Break the Cycle?

There's no single answer — it depends on your income, your expenses, and how aggressively you apply these steps. But most people who follow a clear plan consistently start to feel meaningfully different within two to three months. The emergency fund changes everything. Having even a small buffer transforms your relationship with money and removes the constant background anxiety of financial fragility.

Progress compounds. Each month you stick to the plan, your position improves. Small wins build momentum. And momentum is what ultimately breaks the cycle for good.

The Bottom Line

Living paycheck to paycheck is not a permanent condition — it's a pattern. And patterns can be changed. It starts with clarity about where your money goes, a simple plan for where you want it to go instead, and the consistency to follow through month after month.

You don't need to earn more before you start. You need to manage what you have better — and build from there.

The cycle ends when you decide it ends. Start today.

Are you working to break the paycheck-to-paycheck cycle? What's been the biggest challenge for you? Share in the comments — you're not alone, and your experience might help someone else take that first step.

Related Posts

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

Budgeting & Saving

0 Comments

No comments yet. Be the first to comment!

Leave a comment

Trending News

Newsletter

Stay updated with the latest personal finance and money tips.