What is inflation and how does it affect your Money?

Prices keep rising and your money buys less, that’s inflation. Here’s a plain language to what inflation is, what causes it and exactly how to protect your money from it.

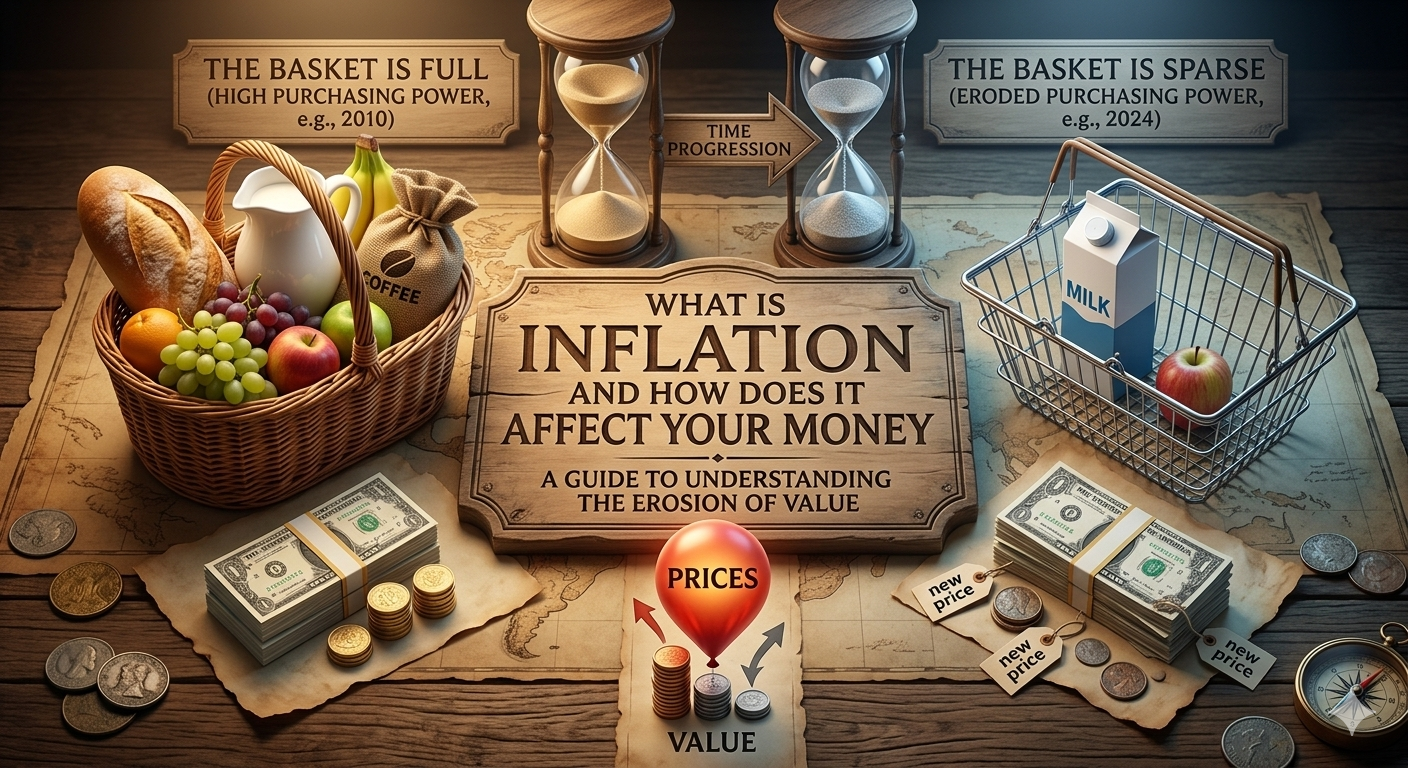

You've probably noticed that things cost more than they used to. A grocery run that cost you $50 a few years ago might now cost $70. Petrol, rent, electricity, food — prices seem to keep going up, and your money seems to buy less and less over time. That's inflation at work.

Inflation is one of the most important economic forces affecting your daily life — yet most people have only a vague understanding of what it actually is, where it comes from, and what it means for their money. This guide breaks it all down in plain language, and more importantly, tells you what you can do about it.

What Is Inflation?

Inflation is the rate at which the general price level of goods and services rises over time — and correspondingly, the rate at which the purchasing power of money falls. In simple terms: when inflation is high, each unit of currency buys fewer goods and services than it did before.

For example, if inflation is running at 5% per year, something that costs $100 today will cost $105 in one year. That doesn't sound dramatic — but over 10 years at 5% annual inflation, that same item would cost around $163. Your money, if left sitting in cash, would buy significantly less than it does today.

Inflation is measured using indices that track the price changes of a typical "basket" of goods and services over time. The most commonly referenced measure is the Consumer Price Index, or CPI — which tracks the prices of everyday items like food, housing, transport, clothing, and healthcare.

What Causes Inflation?

Inflation doesn't happen randomly. It's driven by specific economic forces. The main causes include:

Demand-Pull Inflation

When consumer demand for goods and services outpaces supply, prices rise. Think of it as too much money chasing too few goods. This often happens during periods of strong economic growth, when people are earning and spending more. During the COVID-19 pandemic recovery, for example, pent-up consumer demand surged while supply chains were still disrupted — a textbook recipe for demand-pull inflation.

Cost-Push Inflation

When the cost of producing goods rises — due to higher raw material costs, energy prices, or wages — businesses pass those costs on to consumers through higher prices. The global surge in energy prices following Russia's invasion of Ukraine in 2022 is a clear example of cost-push inflation rippling through economies worldwide.

Built-In Inflation

Also called the wage-price spiral. When workers expect prices to keep rising, they demand higher wages to maintain their purchasing power. Higher wages increase business costs, which leads to higher prices, which leads to more wage demands — creating a self-reinforcing cycle.

Monetary Inflation

When a government or central bank increases the money supply significantly — by printing more money or through expansionary monetary policy — more money circulates in the economy without a corresponding increase in goods and services. This devalues each unit of currency and pushes prices up.

How Is Inflation Measured?

Governments and central banks track inflation through several measures:

- Consumer Price Index (CPI) — the most widely used measure. Tracks the price changes of a standard basket of consumer goods and services over time.

- Producer Price Index (PPI) — tracks price changes from the perspective of producers and manufacturers. Often a leading indicator of future consumer price changes.

- Core Inflation — CPI excluding food and energy prices, which are highly volatile. Used by central banks to get a cleaner picture of underlying inflation trends.

- Personal Consumption Expenditures (PCE) — preferred by the US Federal Reserve as its primary inflation gauge. Broader than CPI and adjusts for changes in consumer behaviour.

What Is Considered "Normal" Inflation?

A small amount of inflation is actually considered healthy for an economy. Most central banks — including the US Federal Reserve, the European Central Bank, and the Bank of England — target an inflation rate of around 2% per year. This level of inflation encourages spending and investment (because money held in cash loses value slowly over time) while keeping prices stable enough for businesses and consumers to plan confidently.

Problems arise at the extremes:

- High inflation (above 5–6%) — erodes purchasing power rapidly, creates economic uncertainty, and hits lower-income households hardest as essential goods become less affordable

- Hyperinflation — extreme, runaway inflation (hundreds or thousands of percent per year) that can collapse an economy entirely. Historical examples include Zimbabwe in the 2000s and Venezuela more recently.

- Deflation — falling prices, which sounds positive but is actually dangerous. When prices fall consistently, consumers delay purchases expecting prices to drop further, economic activity slows, businesses cut costs and jobs, and a deflationary spiral can take hold.

How Does Inflation Affect Your Money?

Inflation touches virtually every aspect of your financial life:

Your Savings Lose Value

If your savings are sitting in a standard account earning 1% interest while inflation is running at 5%, you're effectively losing 4% of your purchasing power every year. Your balance may be the same — or even growing slightly — but what it can actually buy is shrinking. This is called a negative real interest rate, and it's one of the most important reasons why keeping all your money in cash long-term is a poor financial strategy.

Your Cost of Living Rises

Groceries, fuel, rent, utilities, insurance — all of these become more expensive during periods of high inflation. For people on fixed incomes or whose wages don't keep pace with inflation, the real standard of living falls even if the nominal income stays the same.

Your Debt May Become Cheaper in Real Terms

Inflation has one counterintuitive benefit for borrowers with fixed-rate debt: the real value of what you owe decreases over time. If you borrowed $10,000 at a fixed interest rate and inflation runs at 5% for several years, you're repaying that loan with money that is worth less in real terms than when you borrowed it. This is why inflation is generally good for debtors and bad for creditors holding fixed-rate loans.

Interest Rates Rise

Central banks respond to high inflation by raising interest rates — making borrowing more expensive to reduce spending and cool demand. Higher interest rates mean more expensive mortgages, car loans, credit cards, and business loans. If you have variable-rate debt, rising inflation often means your monthly repayments increase.

Your Investments Are Affected

Inflation affects different asset classes in different ways. Stocks have historically outpaced inflation over the long term, making them one of the best inflation hedges for long-term investors. Bonds, on the other hand, are particularly vulnerable to inflation — because their fixed interest payments lose purchasing power as prices rise. Real assets like property and commodities often perform well during inflationary periods.

How to Protect Your Money From Inflation

You can't control inflation — but you can make financial decisions that protect your purchasing power against it.

- Invest rather than hold cash. Over the long term, a diversified investment portfolio in stocks and other assets has historically outpaced inflation significantly. Keeping large amounts of money in cash is a guaranteed way to lose purchasing power over time.

- Consider inflation-protected assets. Some investments are specifically designed to keep pace with inflation — such as Treasury Inflation-Protected Securities (TIPS) in the US, index-linked gilts in the UK, and real estate, which tends to appreciate in value over time.

- Keep debt manageable and fixed-rate where possible. Fixed-rate debt becomes cheaper in real terms during inflationary periods. Variable-rate debt becomes more expensive as interest rates rise.

- Review and renegotiate your income. If your wages aren't keeping pace with inflation, your real income is falling. Advocate for cost-of-living pay rises, explore higher-paying opportunities, or build additional income streams.

- Adjust your budget regularly. During high inflation, your budget from six months ago may no longer reflect reality. Review and update your spending plan regularly to account for rising costs.

- Avoid locking money into long-term low-interest accounts. During high inflation periods, locking savings into accounts with low fixed interest rates means you're guaranteed to lose purchasing power. Look for higher-yield options.

The Bottom Line

Inflation is not just an abstract economic concept — it directly affects what you can afford, what your savings are worth, and how much your investments grow in real terms. Understanding it is the first step to making financial decisions that account for it.

The most important takeaway: money sitting idle in cash loses value over time. The best defence against inflation is to invest wisely, keep your income growing, and make sure your financial plan accounts for rising prices — not just today's prices.

Inflation is a force you can't stop. But with the right financial habits, you can stay ahead of it.

Have you felt the impact of inflation on your daily life recently? Share your experience in the comments — we'd love to hear how you're adjusting your finances to cope.

0 Comments

No comments yet. Be the first to comment!

Leave a comment

Trending News

Newsletter

Stay updated with the latest personal finance and money tips.